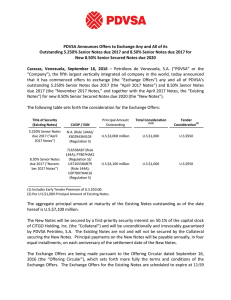

petroleos de venezuela, sa venezuelan national petroleum company

Anuncio