Ejercicio 15.4 - Judge, Pag 660 System: MC3E Estimation Method

Anuncio

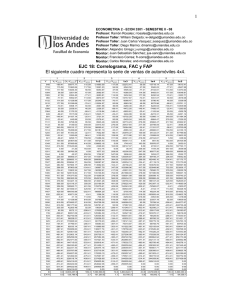

ECONOMETRIA 2 - ECON 3301 - SEMESTRE II - 08 Profesor: Ramón Rosales; rrosales@uniandes.edu.co Profesor Taller: William Delgado; w-delgad@uniandes.edu.co Profesor Taller: Juan Carlos Vasquez; jvasquez@uniandes.edu.co Profesor Taller: Diego Marino; dmarino@uniandes.edu.co Monitor: Alejandro Urrego; j-urrego@uniandes.edu.co Monitor: Juan Sebastián Sánchez; jua-sanc@uniandes.edu.co Monitor: Francisco Correa; fr-corre@uniandes.edu.co Monitor: Carlos Morales; and-mora@uniandes.edu.co EJC 10 B: MINIMOS CUADRADOS EN TRES ETAPAS - Eviews Ejercicio 15.4 - Judge, Pag 660 System: MC3E Estimation Method: Three-Stage Least Squares Date: 08/29/08 Time: 15:20 Sample: 1 20 Instruments: X2 X3 X4 X5 C Coefficient Std. Error C(1) -63.116145 25.760205 C(2) -9.640965 1.751683 C(3) 2.446697 0.279584 C(4) 39.208588 0.772632 C(5) 0.198939 0.002224 C(6) -3.747980 0.322986 C(7) -6.139364 0.304588 C(8) 1.543914 0.100502 C(9) -11.869018 6.277135 C(10) 2.223697 0.340035 C(11) 75.888057 6.292314 C(12) 4.666784 0.413069 Determinant residual covariance 86.1047087 t-Statistic -2.450141 -5.503829 8.751192 50.746814 89.435327 -11.604167 -20.156313 15.362024 -1.890834 6.539608 12.060438 11.297836 Prob. 0.017977 0.000001 Ecuación 1 0.000000 0.000000 0.000000 0.000000 Ecuación 2 0.000000 0.000000 0.064691 0.000000 Ecuación 3 0.000000 0.000000 Equation: Y1=C(1)+C(2)*Y2+C(3)*Y3 Observations: 20 --------------------------------------------------------------------------------------------------------------------------------R-squared 0.994492 Mean dependent var 640.913000 Adjusted R-squared 0.993844 S.D. dependent var 225.746506 S.E. of regression 17.712361 Sum squared resid 5333.371161 Durbin-Watson stat 1.568485 Equation: Y2=C(4)+C(5)*Y1+C(6)*X2+C(7)*X3+C(8)*X4 Observations: 20 --------------------------------------------------------------------------------------------------------------------------------R-squared 0.999375 Mean dependent var 156.536500 Adjusted R-squared 0.999208 S.D. dependent var 39.468057 S.E. of regression 1.110820 Sum squared resid 18.508818 Durbin-Watson stat 1.495382 Equation: Y3=C(9)+C(10)*Y2+C(11)*X2+C(12)*X5 Observations: 20 --------------------------------------------------------------------------------------------------------------------------------R-squared 0.999671 Mean dependent var 904.563000 Adjusted R-squared 0.999610 S.D. dependent var 247.161572 S.E. of regression 4.882223 Sum squared resid 381.377565 Durbin-Watson stat 1.617903 1 de 1